BlackRock Bottom Line – Video Script for Anne Ackerley

Title: From saving to spending: navigating a top retirement concern

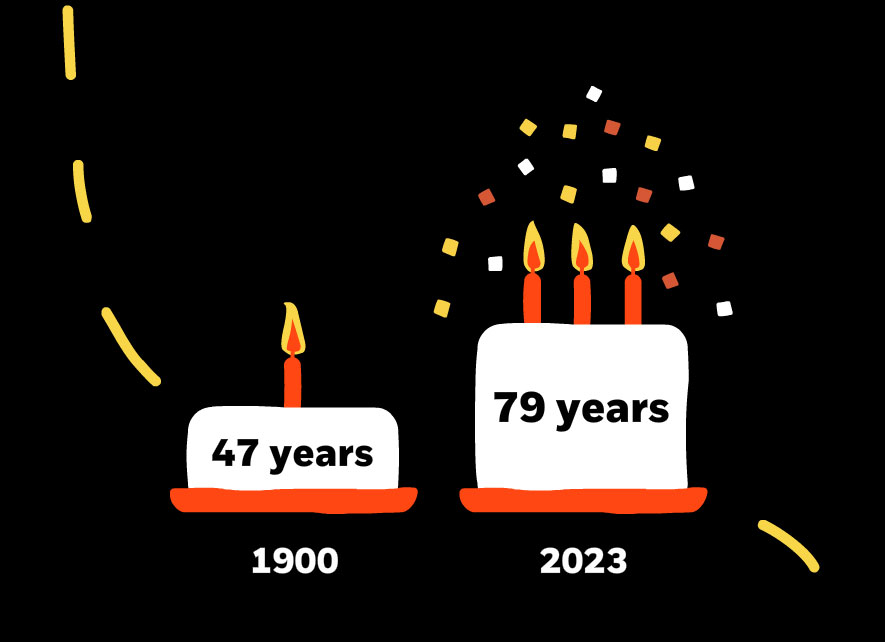

We know the top financial fear around retirement is outliving savings. Yet most retirees still have 80% of their pre-retirement savings two decades into retirement.* It’s a paradox that reveals the major challenge of spending down your nest egg. To solve it, we need to explore new solutions.

Graphic: - Source: BlackRock/Employee Benefit Research Institute (EBRI), December 2020.

BlackRock Bottom Line open

When most people think about “planning for retirement,” it’s usually “savings” that first comes to mind.

And that makes sense because, from the time we start working, it’s a mindset that’s reinforced for decades until, one day, we retire.And then it’s time to spend. But, it turns out, that’s easier said than done.

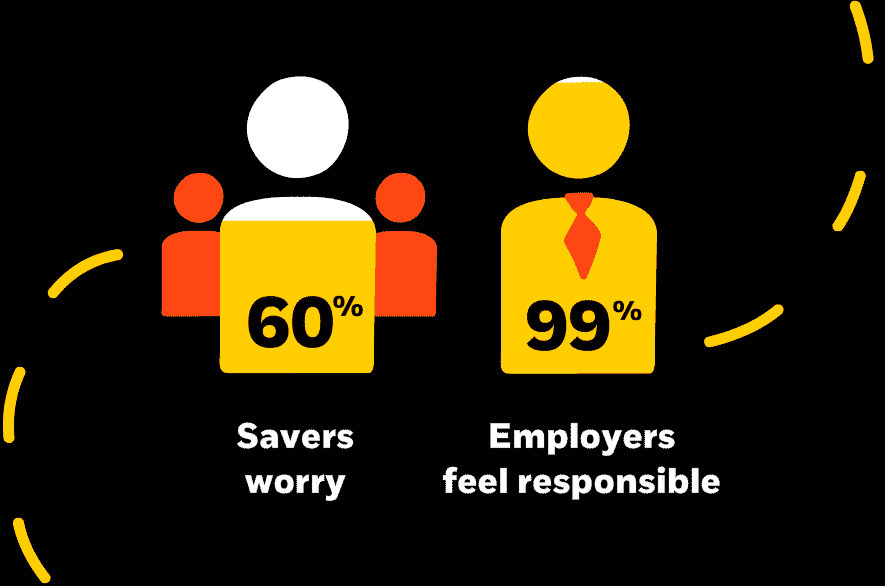

59% of investors say it’s difficult to know how their retirement savings will translate into monthly retirement income.

[Graphic: 59% of investors say it’s difficult to know how their retirement savings will translate into monthly retirement income, BlackRock 2021 DC Pulse]

There are lots of reasons for this, but here are the big ones:

People don’t know how long they are going to live, they don’t know what their expenses are going to be and they don’t know what the market will do.

Yet the burden of figuring this out has increasingly fallen on the individual. Consider the shift from defined benefit plans to defined contribution plans like 401(k)s.

Today, the vast majority of Americans cannot fall back on a pension from their employer. And, while there is Social Security, that wasn’t meant to be the primary source of retirement income.

This is a really hard math problem to solve.

But there is good news. The industry is coming together to address these needs and innovate new solutions to provide retirees with secure income options and greater certainty around their future.

Forward-thinking employers who are moving in this direction can benefit from a more financially secure workforce.

The bottom line is, secure retirement income solutions can help create better retirements. With them, more and more people can feel confident and experience greater well-being across their entire journey.