In this quarterly report the Australian Fixed Income team provide a concise domestic economic, credit and currency outlook for Q1 2025.

Paragraph-1

Paragraph-2

Paragraph-3

Paragraph-4,Accordion-1

Expect a slow easing cycle

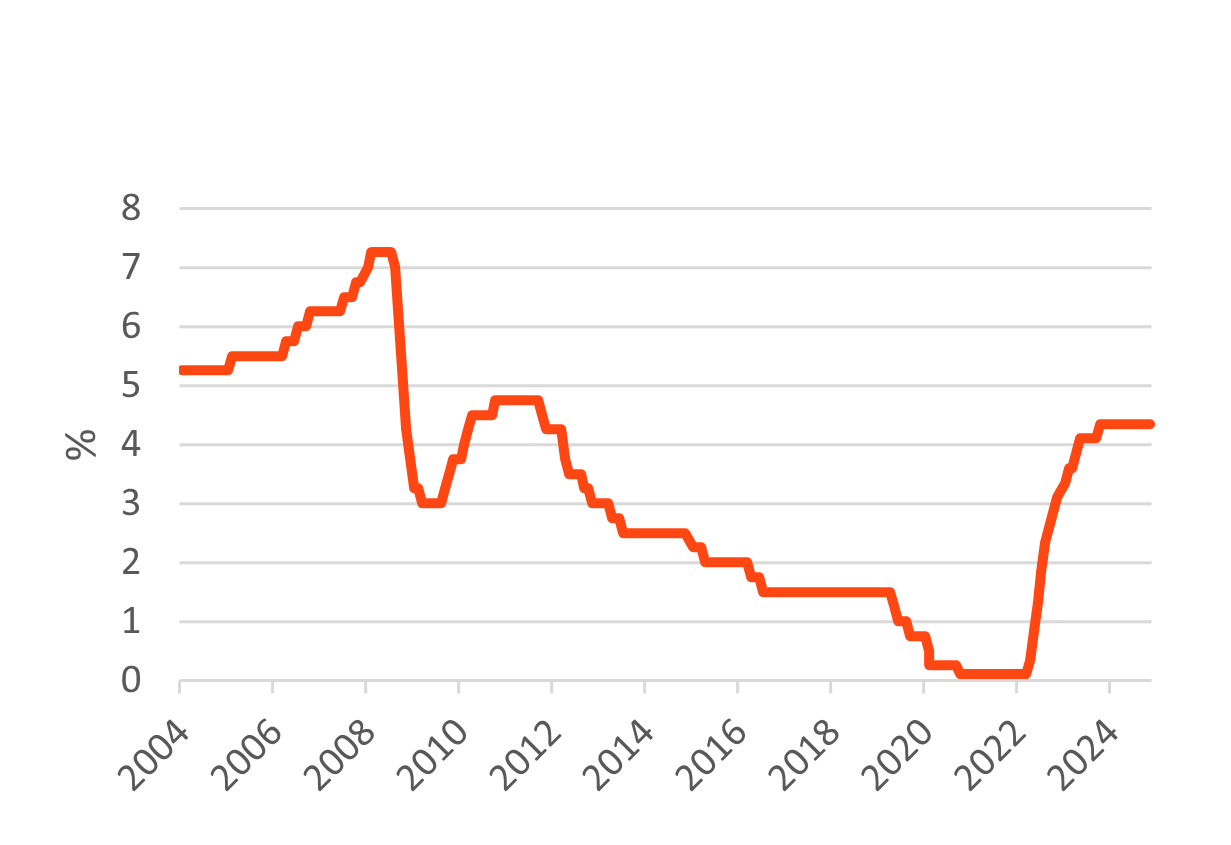

The Reserve Bank of Australia (RBA) kept the official cash rate unchanged at 4.35% in Q424, as we had expected. Our base case remains for the RBA to commence easing in early 2025 at either the February or April meetings depending on how the data evolves over the next few months. Increasing our confidence is the shift to a more dovish stance by the RBA. When the easing cycle here commences, we think the cash rate could converge to 3.60% by the end of 2025.

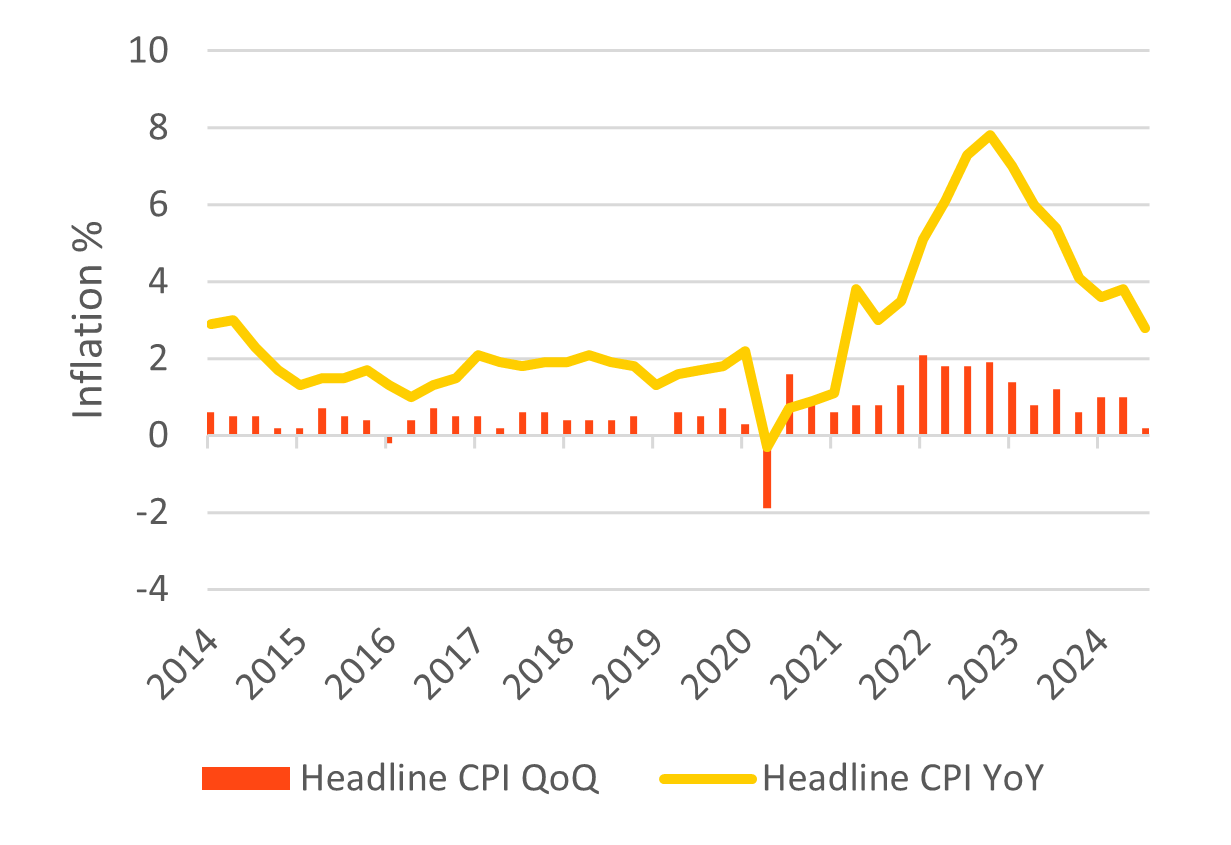

The recent softening in tone and dialling down of rhetoric by the RBA suggests to us they have become more confident that core inflation remains on track to fall in line with their projections. Headline inflation is running at 2.8% YoY, while trimmed mean is 3.5% YoY1. Subsidy effects have delivered a significant and temporary headline disinflation impulse. With a federal election due by May 25, there is a high probability the subsidies will be again extended which will keep headline inflation low. Although the RBA forecasts don’t see core inflation at the midpoint of the 2-3% target band until 2026, the Board doesn’t need to wait to cut rates if they think inflation is “sustainably” falling.

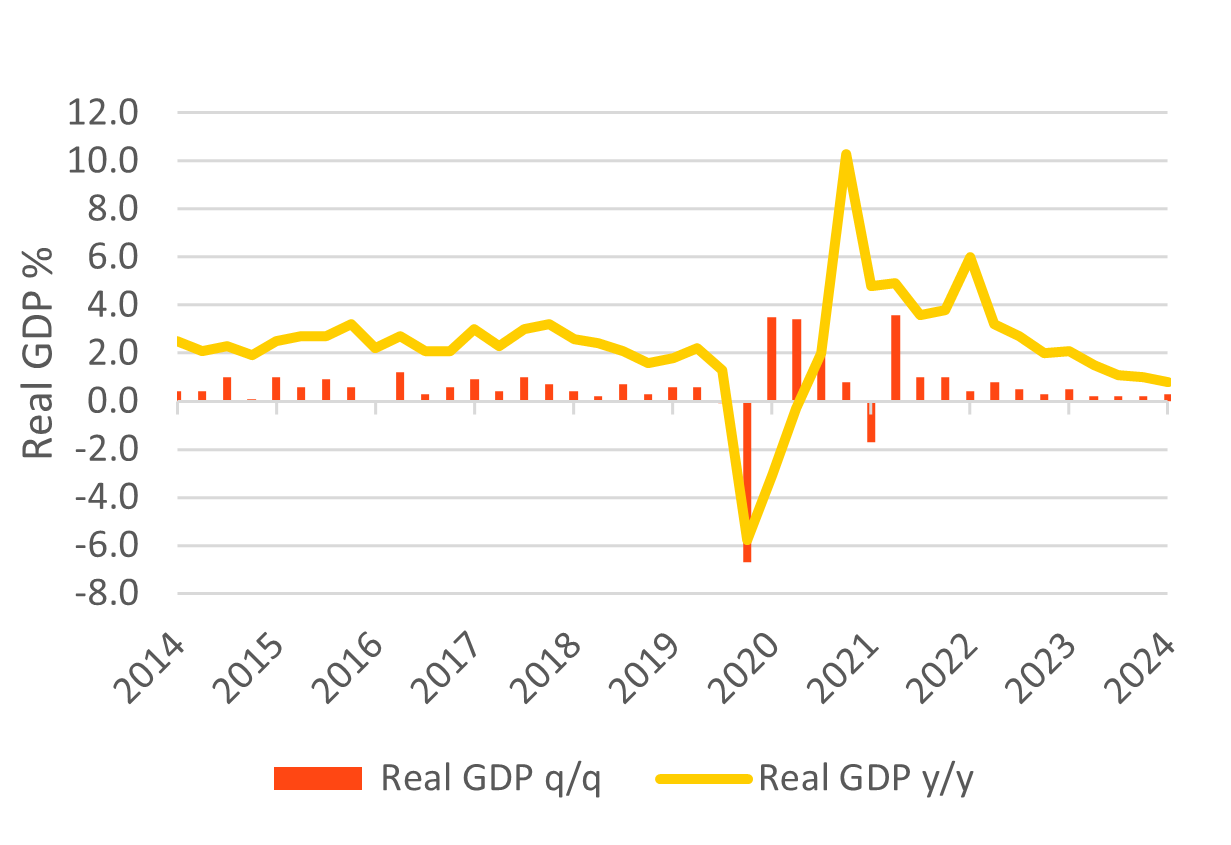

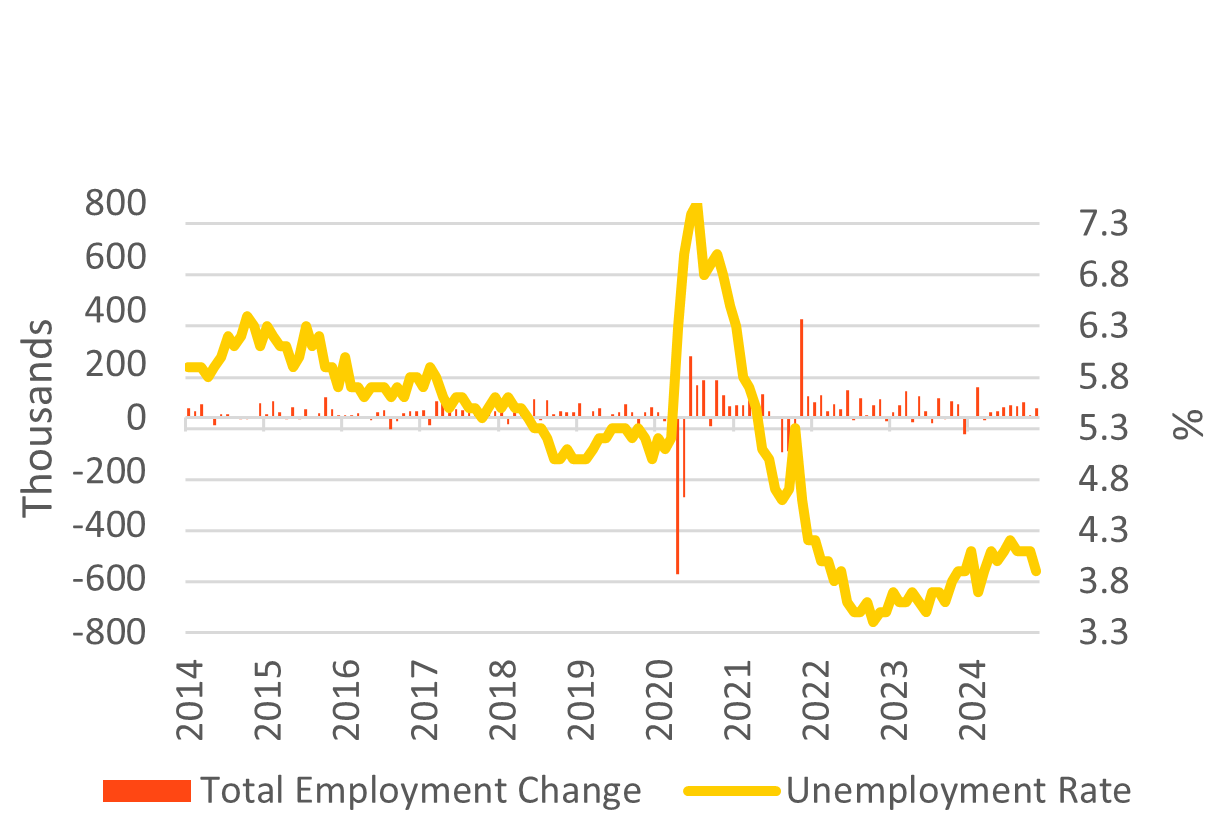

We noted last quarter that labour market conditions were important for the RBA in choosing when to ease policy. While this remains true, very sluggish GDP growth has become an increasing worry for the bank. The RBA acknowledges the labour market is tight and is outperforming versus their expectations. With a current jobless rate of 3.9%, just 0.5% above the post-Covid low of 3.4% (October 2022)1, the risks of a rapid deterioration in labour market conditions has diminished considerably. The RBA expects only a small pick-up in the unemployment rate to 4.4% by Dec-20252.

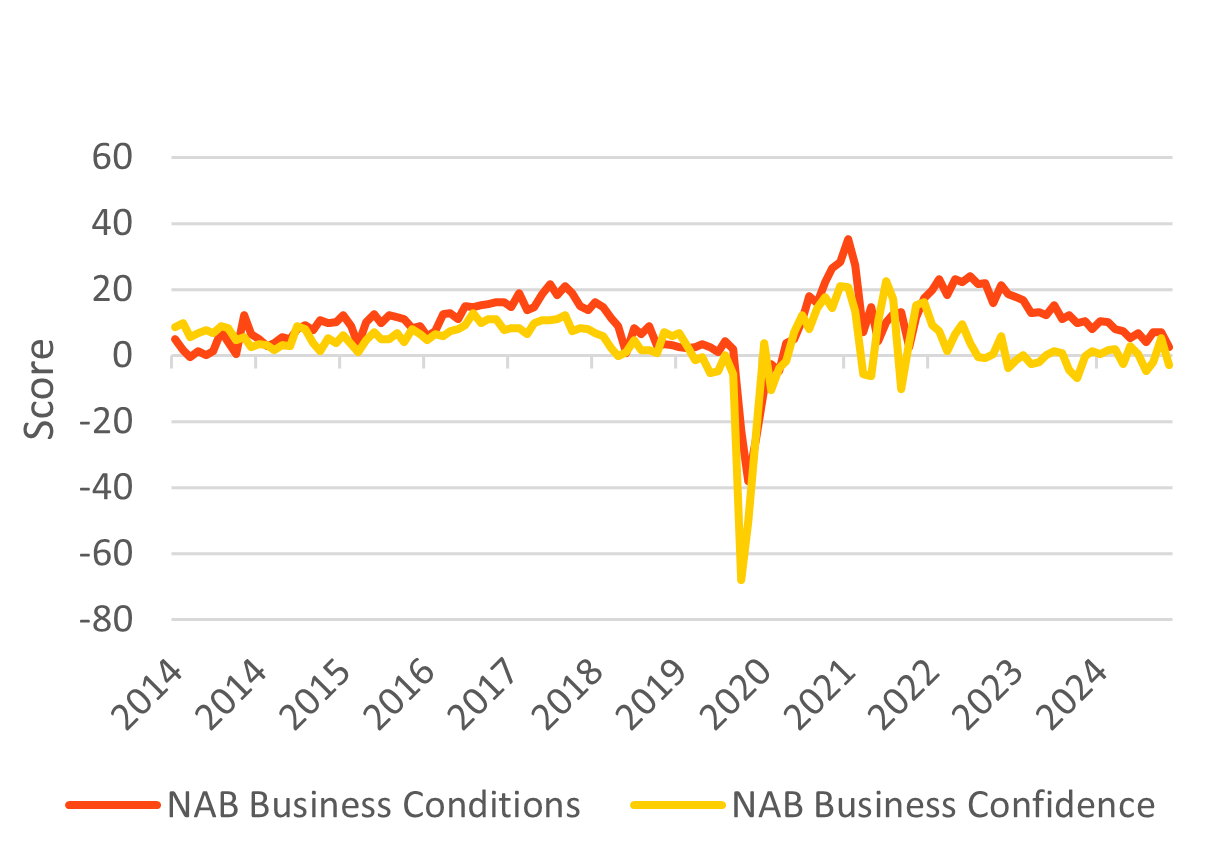

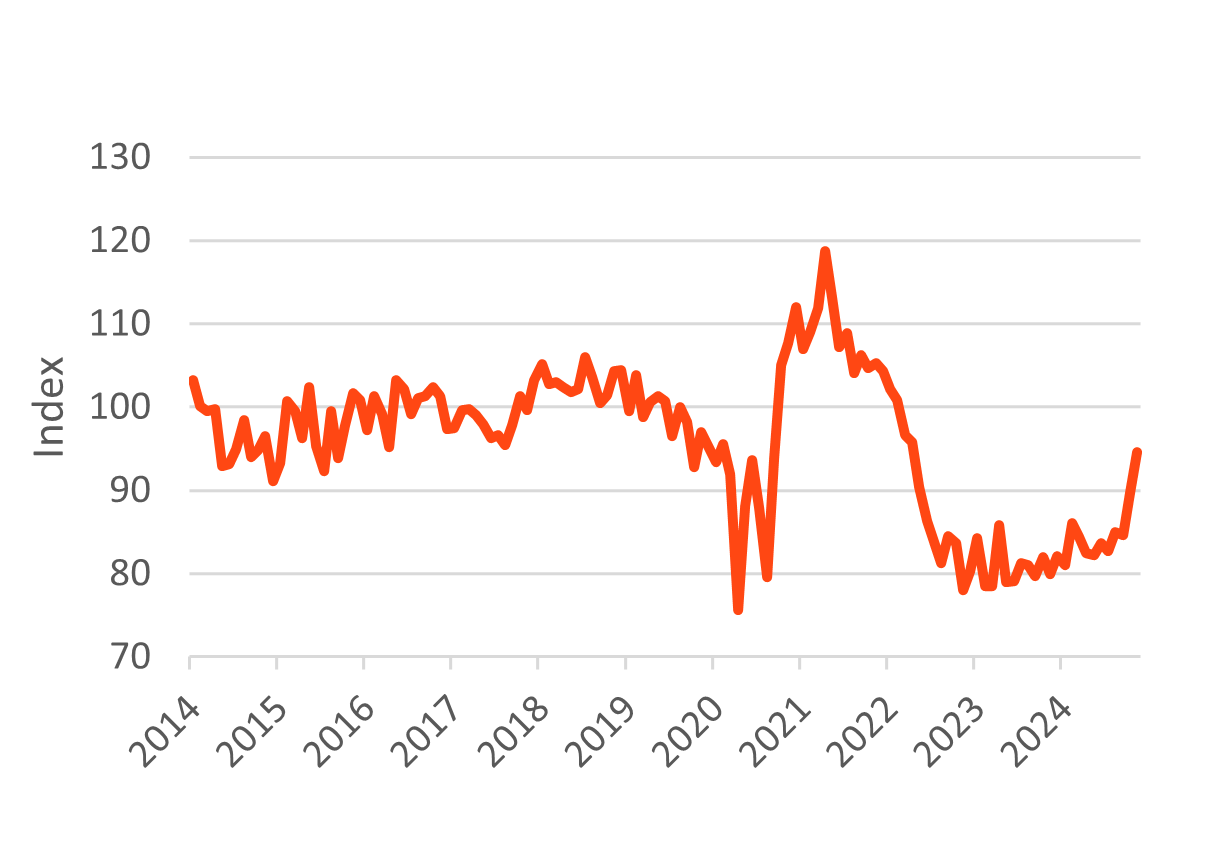

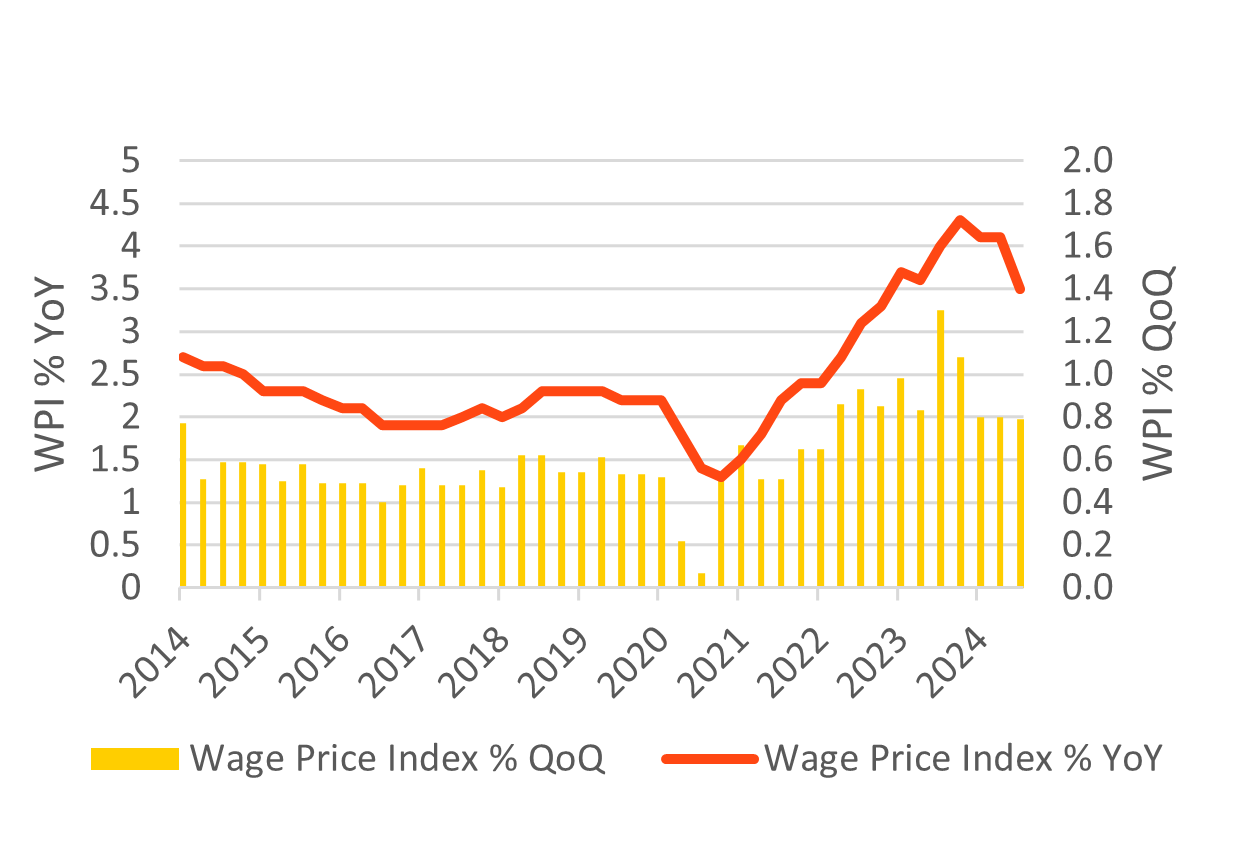

Consumer sentiment is still weak, but we expect conditions to improve moderately through 2025. House prices in the major capital cities are expected to remain under pressure in the short-term, however, rate cuts in 2025 should help to improve affordability metrics. Investment in the housing sector will increase, with the government's ambitious housing target of 1.2 million3 dwellings over five years underpinning supply. Wage price growth is slowing, with the RBA's preferred wage measure – the Wage Price Index (excluding bonus) - running at 3.5% YoY1, the slowest since 2022. The very weak pace of productivity growth remains a challenge for the RBA and limits the degree to which monetary policy can be eased in 2025.

The new structure of the RBA Board becomes effective from 1 March 2025 and based on the membership of the interest rate setting committee, we’d expect to see a smooth transition with respect to their decision-making processes. On the fiscal side, with a federal election in 2025 (by 17 May at the latest), it is expected the government will bring down an early 2025-26 Federal Budget around March. As things stand, the deficit starting point of ~1% of GDP will be a "bit weaker" than previously forecast. With cash deficits baked in over the forecast horizon, there will be increased issuance of government bonds in 2025.

While there remains some uncertainty around what a Trump administration might do with regards to tariffs, recent announcements in China by the Politburo to counter some economic fears are moderately positive for the Australian economy. Chinese policy makers have vowed to embrace a “moderately loose” monetary policy in 2025, and pledged “more proactive” fiscal policy, signalling more rate cuts ahead and shifting from a “prudent” strategy that’s held for nearly 14 years. The RBA has suggested that if China is impacted negatively by tariffs, that could create local disinflationary forces, as it attempts to shift some if its exports to other markets, including Australia.

The first full 25bp rate cut has been priced in for April 25 by the market, with a >50% chance of a 25bp cut priced in as early as February. We think that’s fair pricing given the recent change in tone by the RBA. The implied terminal rate is around 3.60% by the end of 2025, which is close to the RBA’s estimated neutral rate level. We would expect an easing cycle to be a slow and drawn-out affair as the RBA opts against pre-committing to any particular easing path.

Services Inflation is expected to remain sticky

Source: BlackRock, Bloomberg as of 23/12/2024.