Market Insights

Jun 25, 2024|ByJay Jacobs

KEY TAKEAWAYS

- Looking for opportunities beyond today’s leaders: Investors may want to look beyond today’s market leadership to find underappreciated assets poised to benefit from mega forces that can drive long-term growth

- Artificial intelligence (AI): A picks and shovels approach: Integration across industries is driving massive demand for data centers, semiconductors, and raw materials. The AI buildout, projected to continue throughout the decade, will require significant infrastructure investment, presenting investment challenges and opportunities.

- Geopolitics tech and supply chains at the center of a global election year: Geopolitical fragmentation requires an evaluation of overseas dependence and a focus on reshoring. Shifting supply chains and varied demographics create strategic prospects across markets.

LOOKING FOR OPPORTUNITIES BEYOND TODAY’S LEADERS

We believe investors may want to look beyond today’s market leadership to find underappreciated areas that are well-positioned to benefit from powerful secular tailwinds, or mega forces, that can drive long term growth.

In our Thematic Mid-Year Update, we focus on two mega forces where we believe the most compelling immediate opportunities lie: 1) the transformative potential of artificial intelligence (AI) and it’s catalyzation of a historic capex cycle; and 2) the growing impact of geopolitics on trade and technology amid a wave of elections globally.

ARTIFICIAL INTELLIGENCE: A PICKS AND SHOVELS APPROACH

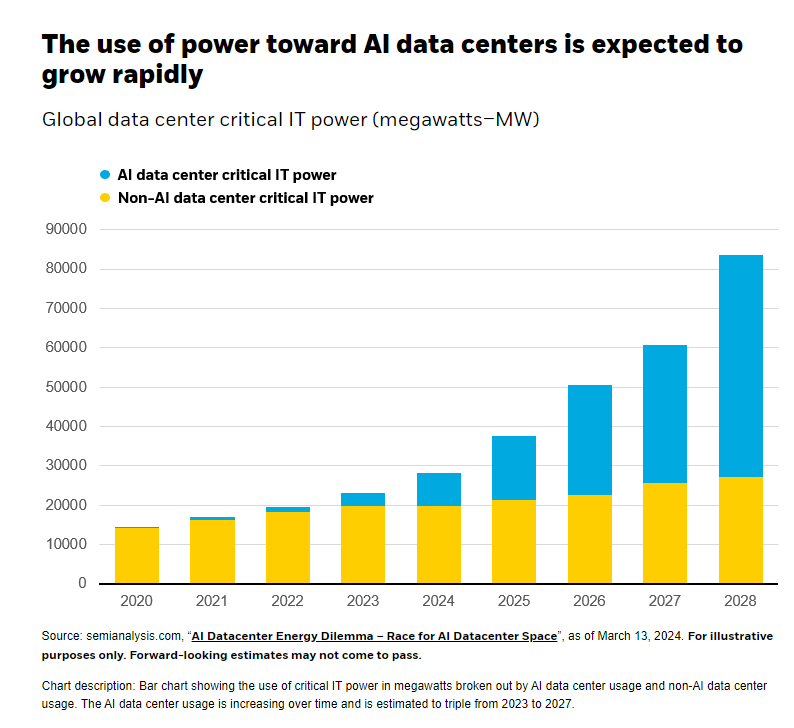

The rapid integration of AI across various sectors is driving a historic capital expenditure cycle, with significant demand for data centers, semiconductors, and certain raw materials, leading to potential opportunities for operators and suppliers of data centers, a broad range of semiconductors, electric power infrastructure, and critical materials.

However, the increasing demand for power and copper, essential for AI data centers and many aspects of energy and digital infrastructure respectively, could pose challenges, necessitating an overhaul of power infrastructure and addressing copper supply deficits.

GEOPOLITICS: TECH AND SUPPLY CHAINS AT THE CENTER OF A GLOBAL ELECTION YEAR

Geopolitical fragmentation is significantly impacting the global economy, reshaping supply chains, and causing a dispersion in U.S. technology stocks due to rising tensions and trade dependencies.

Meanwhile, manufacturing in the U.S. is experiencing a resurgence due to policies aimed at increasing domestic production and reducing reliance on global supply chains, and trade policy changes are creating new opportunities in emerging markets like Mexico and India.

For more insights and to read about our rationale for the recommendations, download the full Thematic Mid-Year Update

Video 1:55

Our 2024 Mid-Year thematic update focuses on two mega forces that are reaching critical inflection points -- the transformative advancements in artificial intelligence and the growing importance of geopolitics.

These mega forces are reshaping the global economy and, as a consequence, are impacting virtually all investors’ portfolios. So how should investors approach these mega forces for the rest of 2024 and beyond?

First, we believe the opportunity today in AI lies less in the digital world and more in the physical infrastructure supporting this technology. Artificial intelligence has transcended buzzword status and is getting rapidly integrated in businesses across the economy, from healthcare to financials and more. Yet as AI adoption takes off, its emergence is creating tremendous and immediate demand for hardware, for digital infrastructure and for power. Semiconductors, data centers, and even raw materials like copper are becoming the picks and shovels critical to AI's growth with data centers alone requiring as much as $1 trillion of investment by 2030.1

Second, geopolitics is reshaping supply chains and public policy, creating select opportunities. Bipartisan efforts in the US to support domestic production and critical industries like semiconductors and automobiles, are poised to drive a renaissance in U.S. manufacturing.

At the same time, select emerging markets like Mexico and India are even benefiting from growing trade and attractive labor pools. And finally, global competition in technology and AI highlights both the vulnerabilities and opportunities of the S&P 500’s largest sector.2

To learn more about these powerful mega forces and how to potentially capture these opportunities in your portfolio, please visit iShares.com/Insights.

Sources

1: McKinsey & Company, “The semiconductor decade: A trillion-dollar industry,” 4/1/22. Forward looking estimates may not come to pass.

2: Sourced from Morningstar as of 6/12/24. The Information Technology sector holds the largest weight in the S&P 500 TR Index, accounting for 31% of the total.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses which may be obtained by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and the general securities market.

Technology companies may be subject to severe competition and product obsolescence.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/developing markets and in concentrations of single countries.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Prepared by BlackRock Investments, LLC, member FINRA.

© 2024 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK and iSHARES are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

Featured Funds-1

Featured Funds-2

Subscribe for the latest market insights and trends

Get the latest on markets from BlackRock thought leaders including our models strategist, delivered weekly.

Please try again

More articles loaded. Use Shift+Tab keys to browse.

Total articles:

ACCESS EXCLUSIVE TOOLS AND INSIGHTS

Explore My Hub, your new personalized dashboard, for portfolio tools, market insights, and practice resources.

Investments

Insights

Practice Management

Tools

Resources

About Us

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/ developing markets or in concentrations of single countries.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and than the general securities market.

Actively managed funds do not seek to replicate the performance of a specified index. Actively managed funds may have higher portfolio turnover than index funds.

Negative changes in commodity markets could have an adverse impact on companies the Fund invests in. The price of the equity securities of companies engaged in mining and the price of the mined metals may not always be closely linked. Worldwide metal prices may fluctuate substantially over short periods of time, so the Fund's share price may be more volatile than other types of investments.

Technology companies may be subject to severe competition and product obsolescence.

Convertible securities are subject to the market and issuer risks that apply to the underlying common stock.

The Fund's use of derivatives may reduce the Fund's returns and/or increase volatility and subject the Fund to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. The Fund could suffer losses related to its derivative positions because of a possible lack of liquidity in the secondary market and as a result of unanticipated market movements, which losses are potentially unlimited. There can be no assurance that the Fund's hedging transactions will be effective.

Small-capitalization companies may be less stable and more susceptible to adverse developments, and their securities may be more volatile and less liquid than larger capitalization companies.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

This material contains general information only and does not take into account an individual's financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial professional before making an investment decision.

The information provided is not intended to be tax advice. Investors should be urged to consult their tax professionals or financial professionals for more information regarding their specific tax situations.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, "BlackRock").

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Bloomberg, BlackRock Index Services, LLC, Cboe Global Indices, LLC, Cohen & Steers, European Public Real Estate Association (“EPRA® ”), FTSE International Limited (“FTSE”), ICE Data Indices, LLC, NSE Indices Ltd, JPMorgan, JPX Group, London Stock Exchange Group (“LSEG”), MSCI Inc., Markit Indices Limited, Morningstar, Inc., Nasdaq, Inc., National Association of Real Estate Investment Trusts (“NAREIT”), Nikkei, Inc., Russell, S&P Dow Jones Indices LLC or STOXX Ltd. None of these companies make any representation regarding the advisability of investing in the Funds. With the exception of BlackRock Index Services, LLC, who is an affiliate, BlackRock Investments, LLC is not affiliated with the companies listed above.

Neither FTSE, LSEG, nor NAREIT makes any warranty regarding the FTSE Nareit Equity REITS Index, FTSE Nareit All Residential Capped Index or FTSE Nareit All Mortgage Capped Index. Neither FTSE, EPRA, LSEG, nor NAREIT makes any warranty regarding the FTSE EPRA Nareit Developed ex-U.S. Index, FTSE EPRA Nareit Developed Green Target Index or FTSE EPRA Nareit Global REITs Index. “FTSE®” is a trademark of London Stock Exchange Group companies and is used by FTSE under license.

© 2024 BlackRock, Inc or its affiliates. All Rights Reserved. BLACKROCK, iSHARES, iBONDS, LIFEPATH, ALADDIN and the iShares Core Graphic are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

iCRMH0824U/S-3770942