2014 Mid-Year Investment Outlook: Life After Zero

3 Jul 2014

As we enter the second-half of 2014, we evaluate the market and question: "What are the implications of the first post-crisis divergence in central bank strategy?" and "What does life after zero (rates) look like?"

BlackRock's overall outlook remains essentially unchanged. We maintain our baseline scenario of "Low for Longer", but recognise that market leadership can change quickly. We believe:

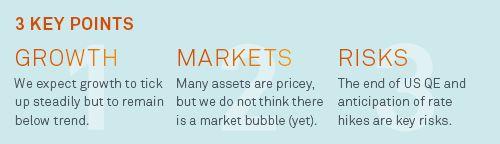

- Valuations are becoming stretched across markets and investor complacency is high. Many asset owners hold similar investments: long credit, long momentum and short emerging markets (EM) risk. This sets markets up for more volatility – especially as the focus shifts from the end of US quantitative easing (QE) to worries about the timing and magnitude of US interest rate hikes.

- The biggest change over the past six months? A brewing crisis in emerging markets has stabilised. Many economies have adjusted and started closing current account deficits, setting the stage for an economic and market rebound. Selection is key, as countries develop at very different speeds.

- The US Federal Reserve has stuck to the mantra of keeping rates low with great conviction – despite mounting evidence the US economy is set to improve. The risk? When it shifts gears, markets are going to notice. Think steeper (and earlier) rate hikes than the market currently expects – but a lower peak federal funds rate than in previous cycles. Also watch out when QE ceases by year-end: The Fed’s reduced bond buying still gobbles up an outsized portion of net debt issuance.

- The European Central Bank (ECB)’s resolve to prevent the eurozone from falling into a deflationary spiral is likely good news for European risk assets. Watch current account balances to gauge competitiveness and the ECB’s manoeuvring room to start an asset purchase programme.

- We are bullish on Japanese equities – despite recent underperformance. Reasons include Godzilla-like QE by the Bank of Japan (BoJ), cheap valuations, structural reforms to boost economic growth, and a rise in domestic investor interest. Expectations on China’s GDP growth may edge down further. Its investment-fuelled economic model is not sustainable. Structural reform is the only way out – but it may push down growth in the short term. Worries about a credit blowout look overdone.

In Singapore, this material is issued by BlackRock (Singapore) Limited (company registration number: 200010143N). Investment involves risks. Past performance is not a guide to future performance. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Any opinions contained herein, which reflect our judgment at this date, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. This material is for informational purposes only and does not constitute an offer or invitation to anyone to invest in any BlackRock fund and has not been prepared in connection with any such offer. Any research in this material has been procured and may have been acted on by BlackRock for its own purpose. The results of such research are being made available only incidentally. BlackRock® are registered trademarks of BlackRock, Inc. All other trademarks, servicemarks or registered trademarks are the property of their respective owners. © 2014 BlackRock Inc. All rights reserved.

BlackRock Investment Institute’s market views

Read it now

Why is innovation so important for investors?

Read it now

Exploring and Exploiting (IL)liquidity

Read it now

Impact of Tighter Financial Conditions

Read it now